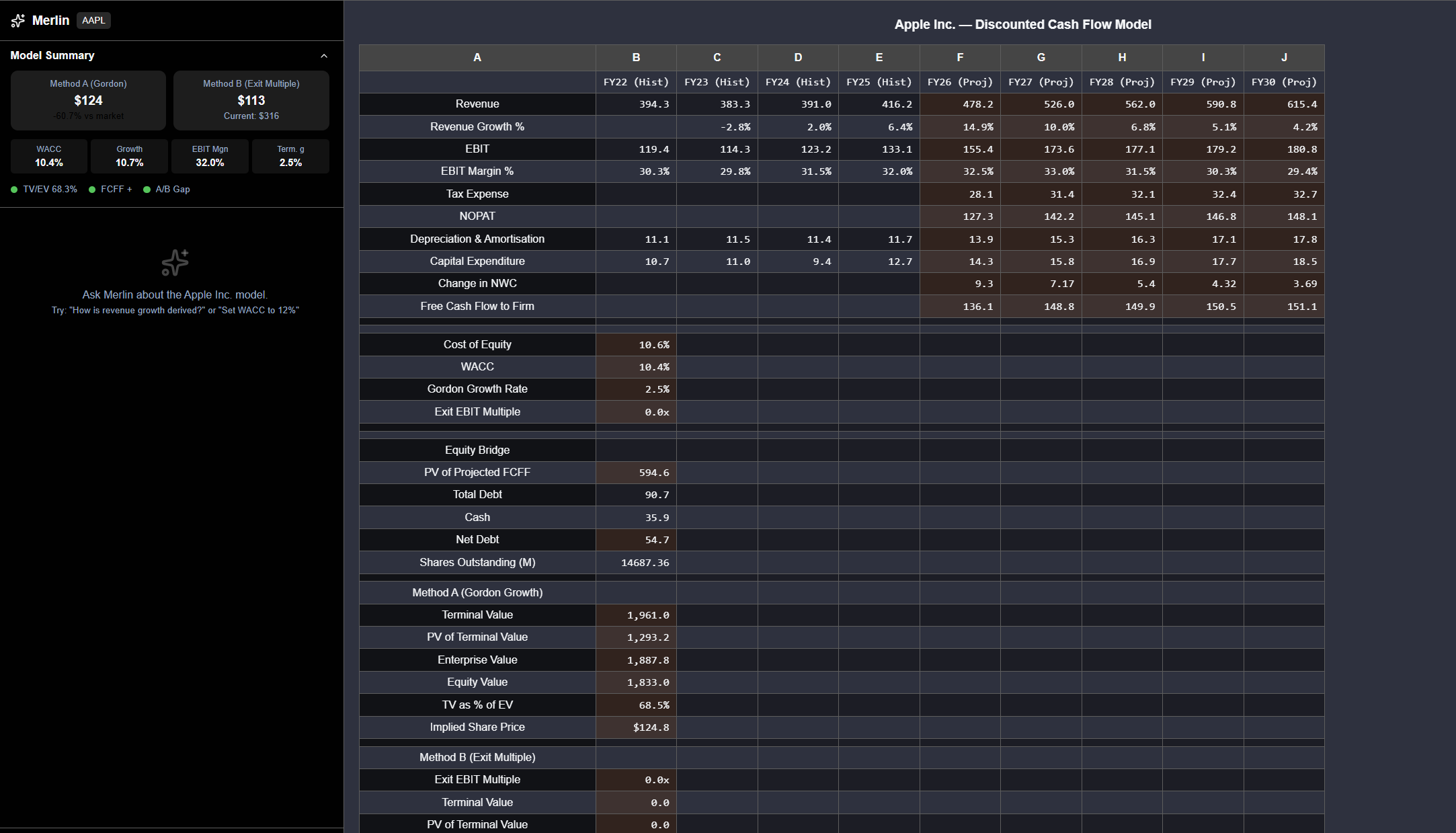

Indian DCF Pipeline

BSE/NSE filings to DCF model in minutes

- Upload a filing, get a full DCF valuation with Excel export

- Two methods (Gordon growth + exit multiple), editable assumptions

- 94.8% accuracy validated across 20+ companies

AI-Powered Equity Research

Type a US ticker or upload an Indian filing—get DCF valuations, 3-statement financials, and earnings analysis in minutes. Every output sourced and exportable to Excel.

Upload a filing. Get a DCF model. Ask the AI anything about it. Every output sourced and audit-ready.

Trusted financial data and AI automation across the investment research cycle.

AI-powered DCF valuations, financial models, document intelligence, and earnings analysis—for Indian and US equity markets.

BSE/NSE filings to DCF model in minutes

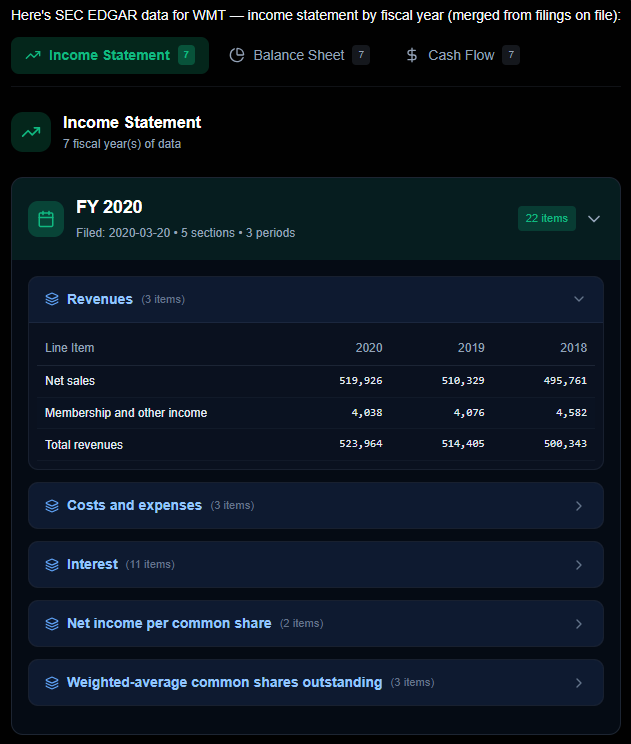

SEC EDGAR, automated

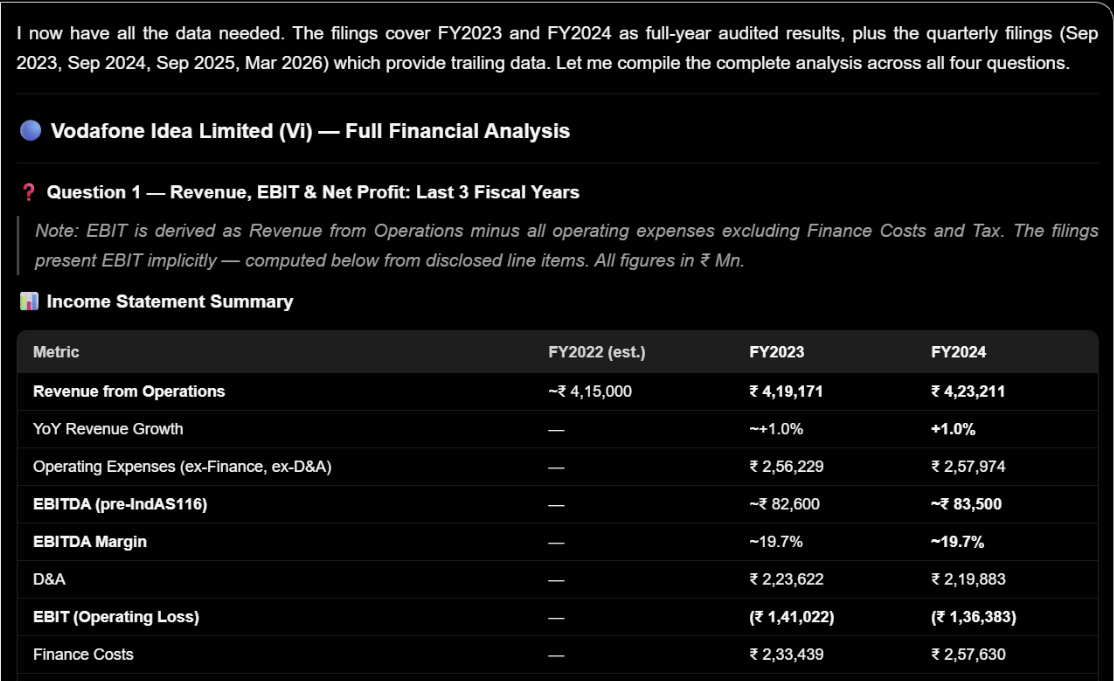

Ask anything, get sourced answers

Bloomberg

$25,000+/year. Doesn't cover Indian equities.

ChatGPT

Summarizes filings. Can't build a model from one.

Accelerate 79ers

Indian DCF + US financials + earnings intelligence. Under $30/mo. Every number sourced.

Whether you manage a fund or invest your own money—get institutional-grade analysis without the terminal cost.

About Vulcan Consulting Group

Vulcan was founded to close the gap between data and decision. We build AI tools that help analysts and investors move faster—with accuracy and transparency at every step.

Sample earnings-call analyses produced with Accelerate 79ers.

Tell us about yourself and we'll show you how Accelerate 79ers can work for you.